How to Get Zepbound Covered by Insurance (and Save Money)

Getting cost effective access to a new medication like Zepbound® (tirzepatide) can feel overwhelming. This guide walks you through step-by-step how to navigate private insurance and Medicaid to get coverage for Zepbound, plus cost-saving tips. We’ll keep it friendly and straightforward, with real-life tips and examples.

Understanding Your Insurance

Private insurance: First, check if your health plan’s drug formulary covers weight-loss drugs. Some plans exclude obesity medications entirely or treat them as “specialty.” If Zepbound isn’t covered by name, it may still be covered under a general GLP-1 (the drug class) or require a formulary exception. If your plan does cover Zepbound, it will likely require prior authorization (PA) – meaning your doctor must prove it’s medically necessary. Remember key terms:

- Deductible: The amount you pay out-of-pocket before insurance starts sharing costsnerdwallet.com.

- Copay: A fixed fee (e.g. $10–$50) you pay for a service or prescriptionnerdwallet.com. Many plans have a set copay for brand-name drugs.

- Coinsurance: A percentage of the cost you pay after meeting the deductible (for example, 20% coinsurance means you pay 20% of the drug cost and insurance pays 80%nerdwallet.comnerdwallet.com).

- Formulary tiers: Insurers group drugs into tiers. Lower-tier (preferred) drugs cost less, higher-tier (non-preferred/specialty) drugs cost more or have higher patient cost-sharemedicalnewstoday.com. Zepbound often ends up in a higher tier for weight-loss plans.

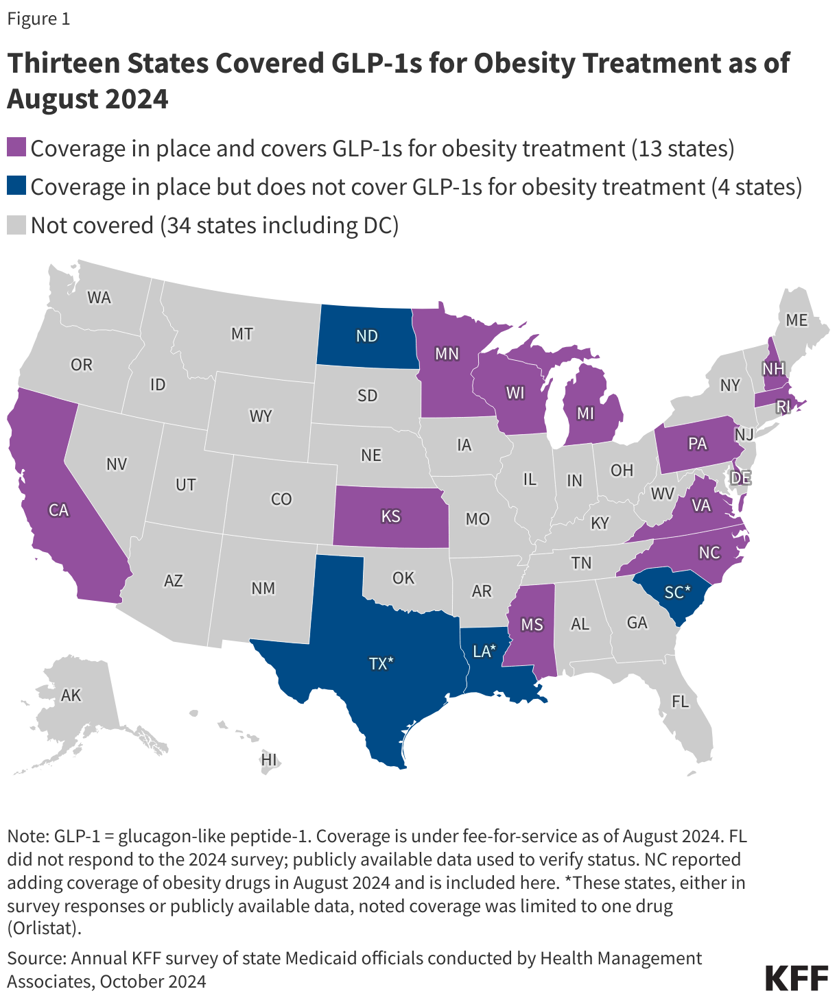

Medicaid: Coverage of weight-loss drugs is optional for state Medicaid programs. As of August 2024, only 13 states cover GLP-1 obesity medications (like Zepbound)kff.org. (See map below.) In those states, fee-for-service Medicaid requires prior authorization and often a high BMI or additional conditions. For example, nearly all states with GLP-1 coverage require PA and many require that the patient’s BMI meet a thresholdkff.org. If you’re on Medicaid, check your state’s formulary or Preferred Drug List (PDL). Even in “coverage” states, Zepbound will have strict rules (BMI ≥30, or ≥27 with a comorbidity like diabetes or hypertension). If your state doesn’t cover it at all, you may need to rely on private insurance or assistance programs.

Figure: States covering GLP-1 weight-loss drugs (purple) under Medicaid as of Aug 2024kff.org. These states allow coverage for drugs like Zepbound, usually with prior authorization and BMI criteriakff.org. (Dark blue states have coverage programs that do not include obesity drugs.)

Steps to Get Prior Authorization

- Talk to your doctor: Explain why Zepbound is needed (e.g. history of overweight/obesity plus related health issues). Your doctor should review your insurance formulary. If the plan requires PA, the doctor’s office will submit the request.

- Provide documentation: When your provider submits a PA, they should include: your weight/BMI, relevant diagnoses, and any trial of other treatments (diet/exercise, other medications). For example, insurers often want to see that you have obesity (ICD-10 E66.x) and possibly a comorbidity like type 2 diabetes (E11.x), hypertension (I10), high cholesterol (E78.5), or heart disease (I51.9)zepbound.lilly.comcontent.naic.org. (See table below for example ICD-10 codes.) This makes the request stronger, since plans often cover weight-loss drugs only for patients with related health issuescontent.naic.org.

- Special documentation: If you have sleep apnea, be sure your doctor notes a sleep study result confirming moderate-to-severe OSA. Zepbound is now FDA-approved for treating OSA in adults with obesityzepbound.lilly.com. For OSA claims, Medicare/Medicaid require OSA as the primary diagnosis and obesity as secondaryzepbound.lilly.com (meaning list OSA first, obesity second). Also document any prior sleep treatments (CPAP use) and lifestyle changes triedzepbound.lilly.comcontent.naic.org.

- Submit the PA: Your doctor can submit the PA through a portal like CoverMyMeds or fax it to the insurance company. CoverMyMeds can help streamline this process, allowing your provider to keep you updated automaticallyzepbound.lilly.com. Be sure they send a copy of the PA and reference number to you.

- Follow up: After submission, check with your doctor’s office or the insurer. Keep the reference number. Many insurers have set timeframes (e.g. 7–14 business days for initial review). If the PA is approved, your insurer will authorize Zepbound for a certain period (often 6–12 months) before re-evaluation.

Appealing a Denial

Denials are frustrating but common. Don’t give up – appeals often succeed. Insurance companies are required by law to allow you to appeal a denial (internal appeal) and even request an independent external review. Here’s what to do if you’re denied coverage:

- Understand the reason: Ask your insurer (in writing) why the request was denied. Common reasons for injectable weight-loss drugs include: “not on formulary,” “not medically necessary,” or “failure to meet prior conditions.” For example, a plan might say your BMI or health history does not meet their criteriamedicalnewstoday.comfindhonestcare.com.

- Gather supporting info: Use your doctor’s help. If the denial says “not medically necessary,” have your doctor write a letter explaining why Zepbound is needed for your health (citing BMI, comorbidities, prior treatments). If it says “experimental,” point out that Zepbound is FDA-approved for obesity and now OSA. If it’s a formulary exclusion, you can request a formulary exception; your doctor can argue that none of the “preferred” options are as suitable for youfindhonestcare.com.

- Write the appeal: Submit an internal appeal to the insurance company within their deadline (often 30–180 days after denial). Include your denial letter, physician letter, medical records, and any relevant studies or guidelines (e.g. NIH obesity criteria). The explanation of benefits (EOB) should list the denial reason – address each point. Medical News Today suggests your appeal should detail your medical history, prior treatments, and why Zepbound is effective for youmedicalnewstoday.commedicalnewstoday.com. For example, you might write, “I have obesity (BMI ___) and type 2 diabetes, and I have tried diet/exercise and other medications without sufficient weight loss. My doctor supports this treatment because weight loss will improve my diabetes control.”

- Timeline: An internal appeal must be filed promptly (typically within 180 days of denial)t1dexchange.org. Once submitted, the insurer must review it (often within 30 days, or 72 hours if urgent). If the internal appeal is denied, you can request an external (independent) review. For Medicare Part D appeals, the internal appeal is up to 120 days, then you can do a Medicare external reviewt1dexchange.org.

- Keep at it: About 40–60% of appeals are successfulfindhonestcare.com. If you win the appeal, the insurer will cover Zepbound. If not, you can still try again if you get new info, or consider alternative options (below). Throughout, stay organized: note the date you filed, who you spoke with, and save all letters and medical documentation.

Leverage Comorbidities

Insurance often covers Zepbound more readily if you have related health conditions. Document any of the following weight-related comorbidities in your medical records: diabetes, hypertension, high cholesterol, sleep apnea, heart disease, or severe joint pain. These can strengthen the “medical necessity” argumentcontent.naic.org. For example, note if you have Type 2 diabetes (code E11.x) or high blood pressure (I10) alongside obesityzepbound.lilly.com. A high BMI plus one of these codes signals to insurers that you have an obesity-related disease. If you have cardiovascular disease, mention it: after all, losing weight with a GLP-1 helps reduce heart risks (semaglutide’s heart-healthy indication is evidence of that). In practice, insurers often require at least one of these codes before approving weight-loss drugscontent.naic.org. Always ask your doctor to double-check that the correct ICD-10 codes (like those in the above table) are on the PA request and any claim formszepbound.lilly.comzepbound.lilly.com.

Key Insurance Terms (In Plain Language)

- Deductible: Amount you pay out-of-pocket each year before insurance starts paying most costs. (If your deductible is $1,000, you must spend $1,000 on covered care firstnerdwallet.com.)

- Copay: A fixed fee (e.g. $25) you pay for a service or prescription. For example, many plans charge a $10–$50 copay for each monthly specialty drug supplynerdwallet.com.

- Coinsurance: The percentage you pay after deductible. For instance, 20% coinsurance means you pay 20% of the drug’s approved cost (and insurance pays 80%)nerdwallet.comnerdwallet.com.

- Out-of-pocket max: The most you’ll pay in a year. After reaching this limit (by paying deductibles, copays, coinsurance), insurance covers 100% of covered servicesnerdwallet.com.

- Formulary (Drug tier): Insurer’s “approved drug list.” Lower tiers cost you less; higher tiers (like brand specialty drugs) cost moremedicalnewstoday.com. If Zepbound is Tier 3 or 4, your copay/coinsurance will be higher unless you hit your out-of-pocket max.

- Prior Authorization (PA): Extra approval step before insurance will pay. You need to get a PA for Zepbound; it’s basically the insurer checking all the boxes (BMI, medical history, trial of other methods).

Knowing these terms helps you understand and anticipate costs. For example, ask your doctor’s office if any cost-sharing (like coinsurance) is due when you pick up Zepbound. Remember, payments to your deductible or coinsurance can be covered by pre-tax HSA/FSA funds.

Saving on Costs

Even with insurance, GLP-1 drugs can be expensive. Here are cost-saving options:

- Manufacturer Savings Card: Lilly offers a Zepbound Savings Card for commercially insured patients. Qualifying members can pay as little as $25 per month (caps apply, often up to $150 off per month)zepbound.lilly.com. Check Lilly’s Zepbound website or ask your doctor about this card. (Note: Not available for Medicare/Medicaid.)

- Patient Assistance Programs: If you have no insurance or very high costs, see if you qualify for Lilly Cares or other manufacturer assistance. These nonprofit programs can provide medications at low or no cost to eligible patients with financial need. Ask your doctor or contact Lilly Cares directly.

- Discount Cards & Coupons: Use pharmacy discount programs like GoodRx, SingleCare, or Optum Perks. These may offer coupons or lower cash prices (for example, Wegovy coupons or Optum Perks often cut costs dramatically)medicalnewstoday.comobesityaction.org. (Note: You can’t combine these with insurance, but if insurance denies coverage, paying cash with a coupon might be cheaper than full list price.)

- Use HSA/FSA: If you have a Health Savings Account (HSA) or Flexible Spending Account (FSA), you can use those pre-tax dollars to pay your share of the drug cost. Prescription drugs for a diagnosed condition are eligible medical expenses under IRS rules.

- Generic alternatives: While not the same drug, some older weight-loss meds are much cheaper. For example, orlistat (Xenical), phentermine, phentermine/topiramate (Qsymia), or bupropion/naltrexone (Contrave) have generic versions and might be covered by your plan. They typically cause less weight loss (5–10%), but they can be a backup if GLP-1s fail. As one obesity specialist notes, cheaper generics can still helpobesityaction.org.

- Advocacy and Assistance: If cost is a barrier, consider clinical trials for new weight-loss treatments (participants often get study medication free). Patient advocacy groups (like the Obesity Action Coalition) also have tips on copay assistance and legislative efforts.

Dealing with No Coverage

If insurance still won’t cover Zepbound, you have options:

- Review Alternatives: Some private plans cover drugs like Mounjaro® (tirzepatide for diabetes) or Wegovy® (semaglutide), but these require a diabetes diagnosis or specific criteria. If you have type 2 diabetes, talk to your doctor about Mounjaro or even FDA-approved GLP-1s for diabetes (Ozempic®). Medicare won’t cover weight-loss GLP-1s, but may cover Ozempic/Victoza if you have diabetes.

- Lifestyle and other programs: Don’t abandon weight loss efforts. Consider structured weight-loss programs (some are covered by insurance as “preventive care”), support groups, or behavioral therapy. These can help bolster your case for medication by showing you’ve tried other methods.

- New Insurance Plans: During open enrollment, check if other employer or marketplace plans cover weight-loss medications. Some employers now cover GLP-1s as a disease-management benefit.

- State Assistance: A few states offer assistance for medication costs if you meet income guidelines. For example, some Medicaid programs will make exceptions or have specialty programs. It’s worth asking your state Medicaid office or a social worker if any waivers exist.

- Stay Informed: Laws are changing. As of 2024, legislation has been proposed to force Medicare to cover obesity drugs. Advocacy groups encourage patients to support bills like the Treat and Reduce Obesity Act (TROA) which could expand coverageobesityaction.org.

Medicaid Coverage by State

The map above highlights how Medicaid coverage for Zepbound (and similar GLP-1 obesity drugs) varies. If you’re on Medicaid, check your state carefully. Even in “covered” states, expect strict PA: most states with coverage require patients to have a high BMI (often ≥40, or ≥35 with health issues) and documented attempts at diet/exercisekff.orgzepbound.lilly.com. For example, California’s Medi-Cal covers Zepbound but only after PA and with obesity-related conditions. The KFF analysis found that of the 13 states covering GLP-1s, 11 required prior authorization and/or a BMI criterionkff.org. If you’re denied, you can appeal through your state’s Medicaid office or managed care plan (similar steps as private insurance).

Zepbound for Sleep Apnea (OSA)

New in 2024: Zepbound is FDA-approved to treat moderate-to-severe obstructive sleep apnea (OSA) in adults with obesityzepbound.lilly.com. This is big because Medicare Part D now covers Zepbound if prescribed for OSA, even though it still can’t pay for weight loss alonemedicalnewstoday.com.

- What you need: A confirmed diagnosis of OSA (usually from a sleep study) plus obesity (BMI ≥30). Your doctor should note these as diagnoses (ICD-10 codes G47.33 for OSA and an E66 code for obesity)zepbound.lilly.comzepbound.lilly.com. It’s crucial that OSA be listed as the primary diagnosis on the prescription/PA form, with obesity as secondary, especially for Medicare patientszepbound.lilly.com.

- Documentation: Include the sleep study report showing an apnea-hypopnea index (AHI) in the moderate or severe range (typically AHI ≥15)zepbound.lilly.com. Also document that you’ve tried standard OSA treatments (like CPAP) and are still symptomatic. Highlight how weight loss medication could improve your OSA and overall health.

- Coverage: If you have Medicare (Part D or Advantage), note that only the OSA indication qualifies; if you don’t have OSA, Medicare will still not pay for weight loss drugsmedicalnewstoday.com. If you have Medicaid (or private insurance), check if OSA is included in their coverage rules. Some plans may follow CMS’s lead and allow coverage for OSA as well.

Tips and Resources

- Be persistent and polite: Always take notes when you call the insurer (who you spoke with, date, reference #). Insurance reps can sometimes override a denial if given more information – it pays to ask questions and stay calm.

- Enlist help: Ask your doctor or clinic staff to take the lead on PAs and appeals. They deal with insurance daily and may know plan-specific requirements. You can even print materials (like this guide!) for them to use.

- Use special funds: If you have an FSA or HSA, these accounts can reduce your actual out-of-pocket cost since contributions are pre-tax. Also consider medical expense deductions on taxes if eligible (talk to a tax advisor).

- Explore coupons: Even if insurance approves, mail-order pharmacies or manufacturer sites sometimes offer coupons to reduce copays. (For example, Wegovy’s site often has coupons that some insurers honor.) Always mention Lilly’s programs when talking to pharmacies or insurers.

- Support groups: Online communities (like r/Zepbound on Reddit) are full of others going through this. They share tips on how they got PA approved, sample appeal letters, and up-to-date info on insurance policies. Just remember: every plan is different, so use those stories as ideas, not guarantees.

Throughout this process, keep focused on your health goals. Losing even 5–10% of body weight can dramatically improve diabetes, blood pressure, sleep apnea, and heart health. When you appeal or discuss with your doctor, emphasize your personal health struggles (e.g. inability to control blood sugar, CPAP intolerance, joint pain). Insurance will cover Zepbound if it’s clearly medically necessary for you.

We hope this guide makes the journey a little easier. With persistence, the right documentation, and these tips, you stand the best chance of getting Zepbound covered by insurance – or finding another affordable path to the care you need.